An Update on My Big Zillow Bet

Over the last few days my DMs have been flooded with same variation of the following question:

“Will you be trimming your Zillow position?”

For my own benefit, as well as those interested in tracking my portfolio, I am sharing my rationale for not trimming in order to 1) clarify my thinking, 2) make an explicit decision, 3) give myself primary text to learn from when I inevitably look back at this crossroad in the future.

Disclaimer: nothing here is investment advice! This decision is deeply personal to me and no one else. The only reason I share it is because I believe in the concept of open-source investing.

How it started…

I started building my Zillow position in April of 2018 after the company announced it would officially enter the iBuying business competing directly with Opendoor.

A year later when Zillow announced Rich Barton would be returning to serve as the company’s CEO, I increased the size of my position to ~$250k, over 75% of my net worth at the time.

This post is intended to explore the psychological aspect of making, and holding, such a highly concentrated bet. I have written about my thesis elsewhere (see examples here, here, here, and here) so I won’t rehash it now despite it being necessarily important. Here is a brief elevator pitch:

Zillow sits at the most valuable position in the residential real estate value chain as the first place most consumers go to buy or sell a home.

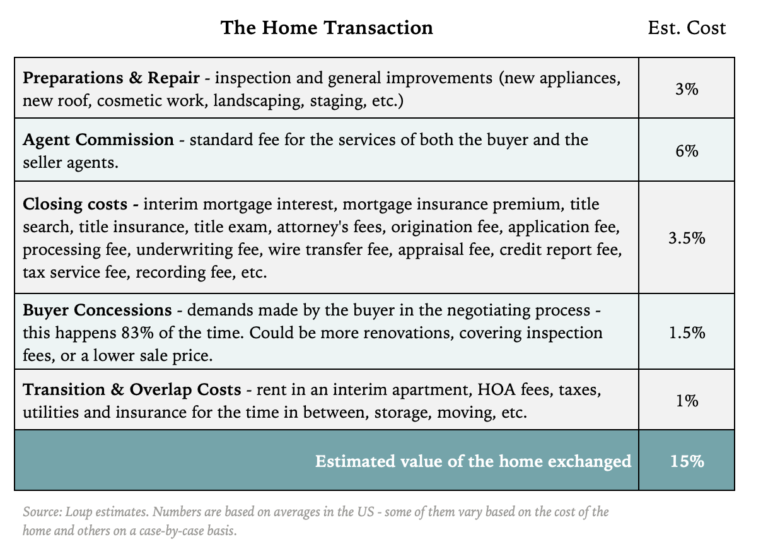

Customers pay as much as 15% in fees during and adjacent to the home transaction (e.g. agent commissions, title, mortgage, inspections, renovations, closing and moving costs). If $1.5 to $2 trillion dollars of residential real estate changes hands every year, customers are paying in the neighborhood of $225 to $300 billion in fees. That’s a massive opportunity.

iBuying was the Trojan horse that allowed Zillow to insert itself into the center of the transaction, where it can simplify the process, bundle many of the fees, as well as reduce the overall cost and friction for the end customer.

{kind=link}

I have also written about the rationale for making such a large and concentrate bet in my post, Allow Me To Reintroduce Myself.

Simply put, I’m looking to hit a home run. I believe Zillow represents an asymmetric opportunity. No doubt I could play it safe, buy an index fund, and likely be sitting on a ~$5M portfolio by the time I’m 60 years old. Personally, I’d much rather take a crack at materially changing the trajectory of my personal finances while I’m young enough to enjoy it. As obnoxious as this sounds, I can afford to lose it all this early in my life. I have high-paying job and no other financial obligations.

How it’s going…

During the time that I have owned Zillow shares, the stock price has seen four major selloffs of 59%, 27%, 42%, and 64% respectively. I know there will be more to come.

I can’t stress this point enough. It was extremely painful to watch a position that made up such a significant percentage of my net worth drop this much. To make matters more difficult, many prominent investors including Steve Eisman, Jim Chanos and numerous highly respected accounts on FinTwit expressed extreme skepticism about Zillow’s business model. Many of these critics remain as skeptical as ever.

I am not here to make the case that they are wrong and I am right. I view the future as but one of a range of potential outcomes, acknowledging there are scenarios where I am directionally correct and others where the skeptics are. Where we differ is the probabilities we assign to the range of outcomes.

That said, I mention the skeptics to illustrate how hard it has been to maintain my conviction over the last two years. Investors who are more experienced and more sophisticated than I am have forced me to consider the real possibility that I am spectacularly wrong. That level of self-reflection is something most people, never mind most investors, are unwilling to do because it is not fun.

How it will end…

I don’t know how this will end.

What I do know is that I am am comfortable seeing my bet through to the end regardless of the path it takes to get there. (Assuming my long-term thesis remains intact.)

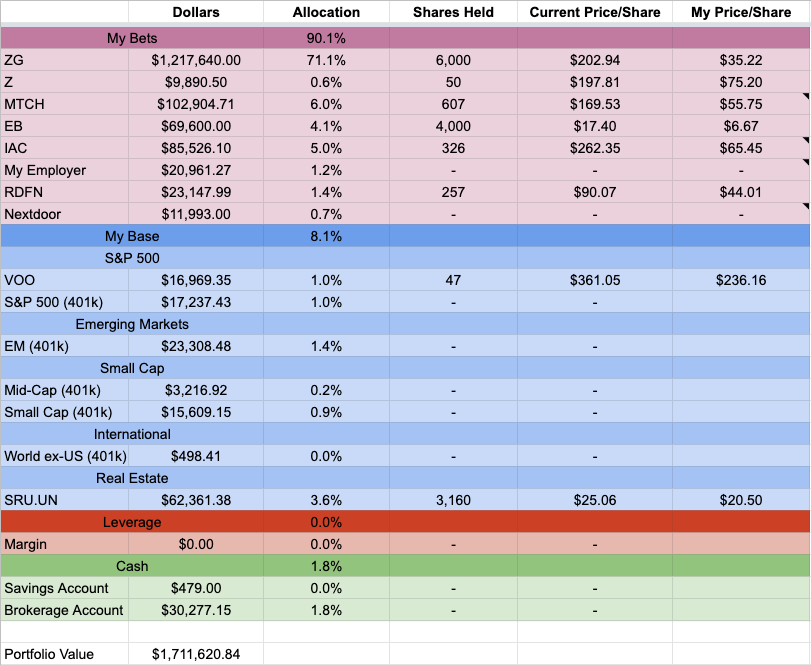

This is how my portfolio looks as of writing these words:

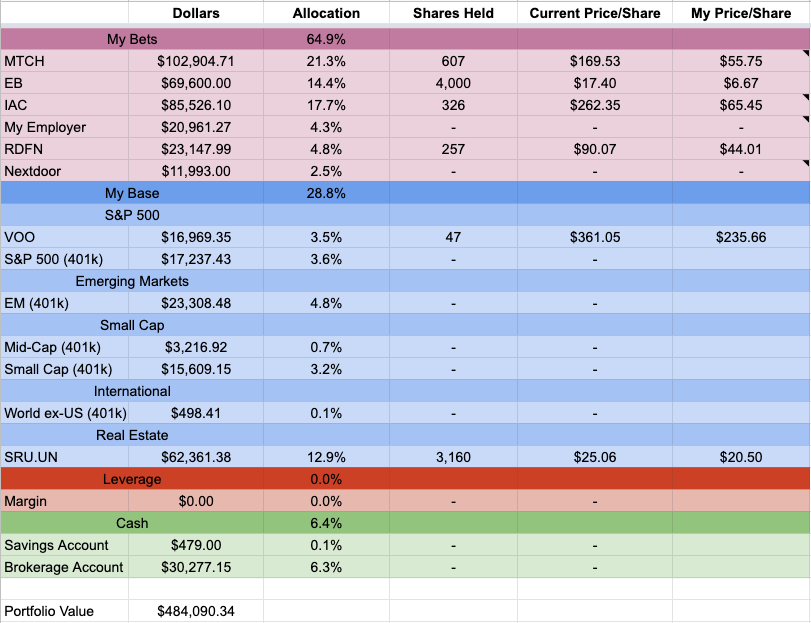

Let’s say I am wrong about Zillow and the company is a zero, absolutely worthless.

This is how that same portfolio would look:

I am 29 years old. I am lucky to have high-paying job working in software sales. If Zillow were to go to zero, my personal finances won’t require anyone’s pity.

I would have lived through an interesting case study, something most people my age only read about in business school for about the same cost as my initial investment.

If I were to trim my position today my life would not materially change. But if I were to trim, and my thesis was ultimately proven to be correct, I would live the rest of my life with regret.

Alternatively, when I am on my deathbed I am not going to regret betting on myself even if I am proven wrong in the end.

So, should I trim my Zillow position?

I don’t think that’s the right question.

The question I am asking myself is whether or not I still believe in my thesis?

And the answer to that question is yes.