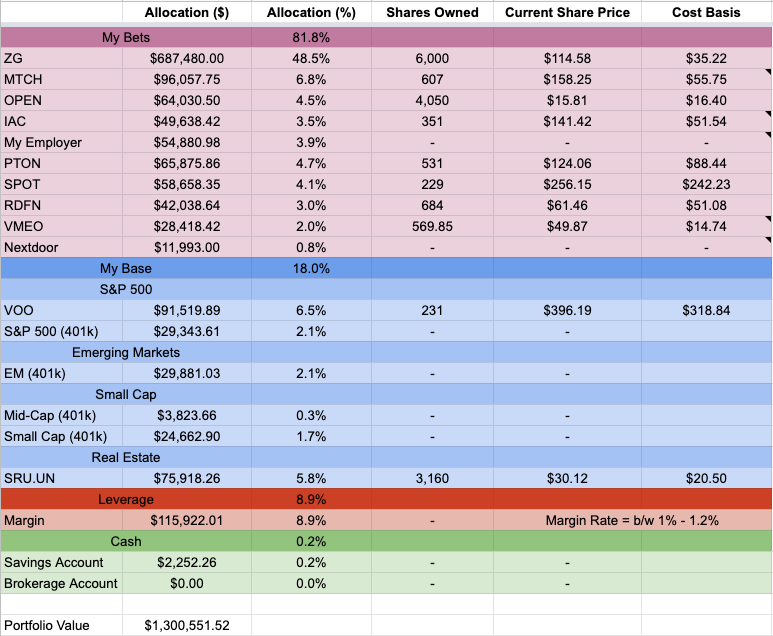

Mid-Year Portfolio Update

Investing Journal - Post #7

This review is mostly for me since the blog serves as my personal investing journal. But if you’d like to discuss any of the below please reach out via Twitter.

Zillow / Opendoor / Redfin

The Opportunity:

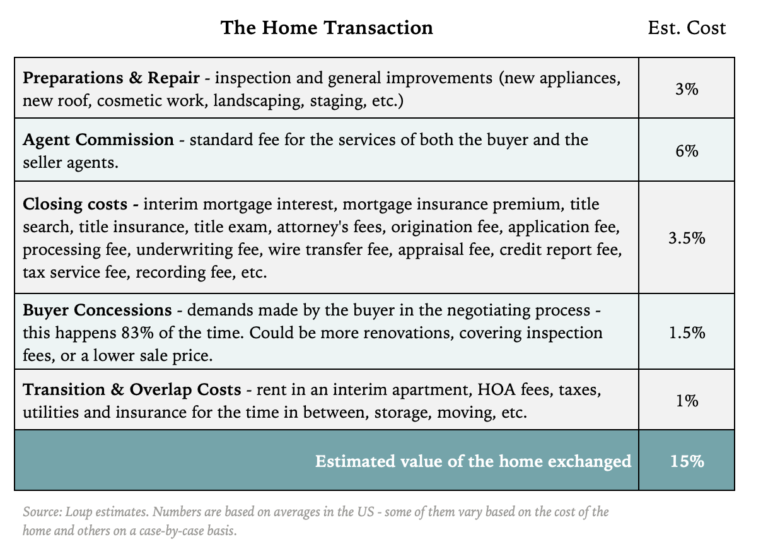

Customers pay as much as 15% in fees during and adjacent to the home transaction (e.g. agent commissions, title, mortgage, inspections, renovations, closing and moving costs). If $1.5 to $2 trillion dollars worth of residential real estate changes hands every year, customers are paying in the neighborhood of $225 to $300 billion in fees. That’s a massive opportunity in a highly fragmented industry.

Companies like Zillow, Opendoor, and Redfin have inserted themselves into the center of the transaction, where they hope to simplify the process, bundle many of the fees, as well as reduce the overall cost and friction for the end customer.

The beauty of this setup is that Zillow, Opendoor, and Redfin are each attacking the opportunity from different angles giving investors multiples path to success.

{kind=link}

The Case for Zillow:

Zillow sits at the most valuable position in the residential real estate value chain as the first place most consumers go to buy or sell a home. Its website and app gets 3.5x more traffic than Redfin and 1.8x the traffic of Realtor.com.

Rich Barton and Lloyd Frink are proven executives. The duo has exhibited both a willingness to adapt and a capacity to suffer during Zillow’s transition from lead gen advertising business to transactional marketplace.

Zillow effectively has call options on Opendoor’s and Redfin’s business models.

The Case for Opendoor:

By taking a completely orthogonal approach to home buying and selling (iBuying), Opendoor has made more progress disintermediating real estate agents than both Zillow and Redfin.

Opendoor is the leading iBuyer in terms of both volume and contribution margin thanks to a seemingly superior pricing model. If this pricing advantage proves durable, Opendoor has a reasonable path to become the dominant real estate marketplace.

The Case for Redfin:

Redfin is the third most trafficked real estate marketplace with W2 employees serving as agents.

Redfin’s in-house agents mean the company has control over the entire process but revenue growth will be linear as long as agents aren’t replaced by software. The catch 22 of Redfin’s bull thesis is that if agents are replaced by software, Zillow should be able to co-opt the model with a bigger audience.

Match Group

A reverse DCF implies lofty expectations but Match Group is a prime example of an asset that I wont sell or trim on valuation alone.

The competitive dynamics remain attractive and there’s plenty of green field to pursue as more of the dating experience moves online, even if I can’t specifically underwrite it in a DCF model.

IAC

I’m betting on proven capital allocators and business operators at a fair price.

Some investment decisions are that simple.

Peloton

Peloton is a fantastic company. I’m not going to do a deep dive here as there are other analysts who do a superior job of breaking down the business.

But if there’s one thing I can contribute the the conversation, it’s a lesson I learned from the iPhone. Never underestimate the power of integrated hardware and software. That pairing, along with a combo platter of a first-mover advantage and scale benefits, give Peloton quite the moat against competitors.

Peloton’s TAM has also significantly expanded compared to when the company went public in 2018. Remote work has moved firmly into The Overton Window meaning knowledge workers now have the freedom to spend a large chunk of the work week at home.

Oh, I also like investing in cults.

Spotify

Over the last decade bargaining power in the music industry has slowly, but surely shifted away from record labels.

“When leverage genuinely shifts from party A to party B, it shifts far more profoundly than anyone realizes in the moment.”

- Peter Thiel

While artists have reclaimed some of the labels’ profit pool for themselves via alternate revenue streams, Spotify’s grip over the growing audio ecosystem is getting stronger.

In the words of @LongHillRoadCap, “the beautiful thing about Spotify is it becomes a better, more profitable, more durable, and more inevitable business as it grows.”

Nextdoor

When Nextdoor completes its merger with Khosla Ventures Acquisition Co. II, it will mark the first IPO of a private company I'm invested in. Cool, cool. I’m crossover investor now.

I initially characterized the investment as a bet on Sarah Friar, and because Nextdoor is a social network with a few attractive qualities:

Unique online & offline component

High barrier to entry as the network is difficult and time consuming to build

Distinct audience that has little overlap existing with social networks

Prior to the SPAC deal announcement, I wrote that I wish I owned more Nextdoor stock. Now I have the opportunity to do so.

Vimeo

I wish I knew what to do with these shares. Vimeo isn’t a big enough position to really help/hurt my portfolio but I regretfully haven’t down enough work to make an informed buy more vs sell decision. It’s on my to-do list.